Filed by Stratasys Ltd.

(Commission File No. 001-35751)

Pursuant to Rule 425 of the Securities Act of 1933

and deemed filed Pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Form F-4 No. 333-272759

Subject Company: Desktop Metal, Inc. (Commission File No. 001-38835)

The following presentation was made available on the Stratsys Ltd. investor relations website (https://investors.stratasys.com/) on September 14, 2023.

Protecting Value for Stratasys Shareholders S e p t e m b e r 2 0 2 3

2 Key reasons for rejection of DDD’s proposal 1 3D System’s (“DDD”) current proposal significantly undervalues Stratasys (“SSYS”) ⚫ The revised proposal reflects a nominal value of $15.26 per share for Stratasys, representing a premium of only 15% as of September 11, 2023, and only 3% premium to the unaffected closing stock price of Stratasys shares as of May 24 ⚫ Proposal is ~35% lower than the value implied by 3D Systems’ July 13, 2023 proposal ⚫ DDD continues to trade at a premium multiple to SSYS despite declining growth and significantly lower margins Serious concerns about DDD’ short - to - medium - term growth prospects ⚫ DDD reported Q2 results on August 9, 2023, missing its own guidance as well as street expectations, and significantly guiding down 2023 fiscal estimates ⚫ Sales to Align Technologies (23% of DDD revenue) are declining and at high risk 2

3 Key reasons for rejection of DDD’s proposal 4 Net synergy potential is materially lower than what DDD is broadcasting ⚫ DDD was unable to furnish any credible support backing its claim of cost synergies of more than $110M ⚫ Based on analysis performed by a leading consulting firm, we estimate cost synergies of $74 – 88M ⚫ Based on detailed work performed by Stratasys management and independent advisors, there will be approximately $50mm of annual negative revenue synergies Structural challenges to a path to attractive profitability 3 ⚫ DDD’s portfolio already operates at gross margins that are significantly below the gross margins of Stratasys: DDD is at 39%, while Stratasys is at 49% ⚫ Consensus 2023 estimates for DDD’s EBITDA remain negative ⚫ If DDD’s dental business declines due to Align shifting its sourcing, DDD’s profitability could fall even further and weigh down the margins of a combined company

4 Key reasons for rejection of DDD’s proposal 6 Serious concerns regarding the ability of DDD’s management team to run a combined company ⚫ DDD management has repeatedly missed estimates and lowered guidance; SSYS’ management team, in contrast, has delivered superior performance ⚫ Skepticism regarding DDD management’s ability to deliver synergies based on lack of track record ⚫ The combined entity will have a weak pro forma balance sheet - $57M in cash and $460M in debt Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months ⚫ Likely require a lengthy and extensive regulatory review process, an extended duration to closing and significant costs to obtain the required regulatory approvals ⚫ This extended timeline to closing creates significant risks of employee attrition and channel disruption 5

Agenda 5 DDD’s current proposal significantly undervalues SSYS 1 Serious concerns about DDD’s short - to - medium - term growth prospects 2 Structural challenges to a path to attractive profitability 3 Net synergy potential is materially lower than what DDD is broadcasting 4 Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months 5 Serious concerns regarding the ability of DDD’s management team to run a combined company 6

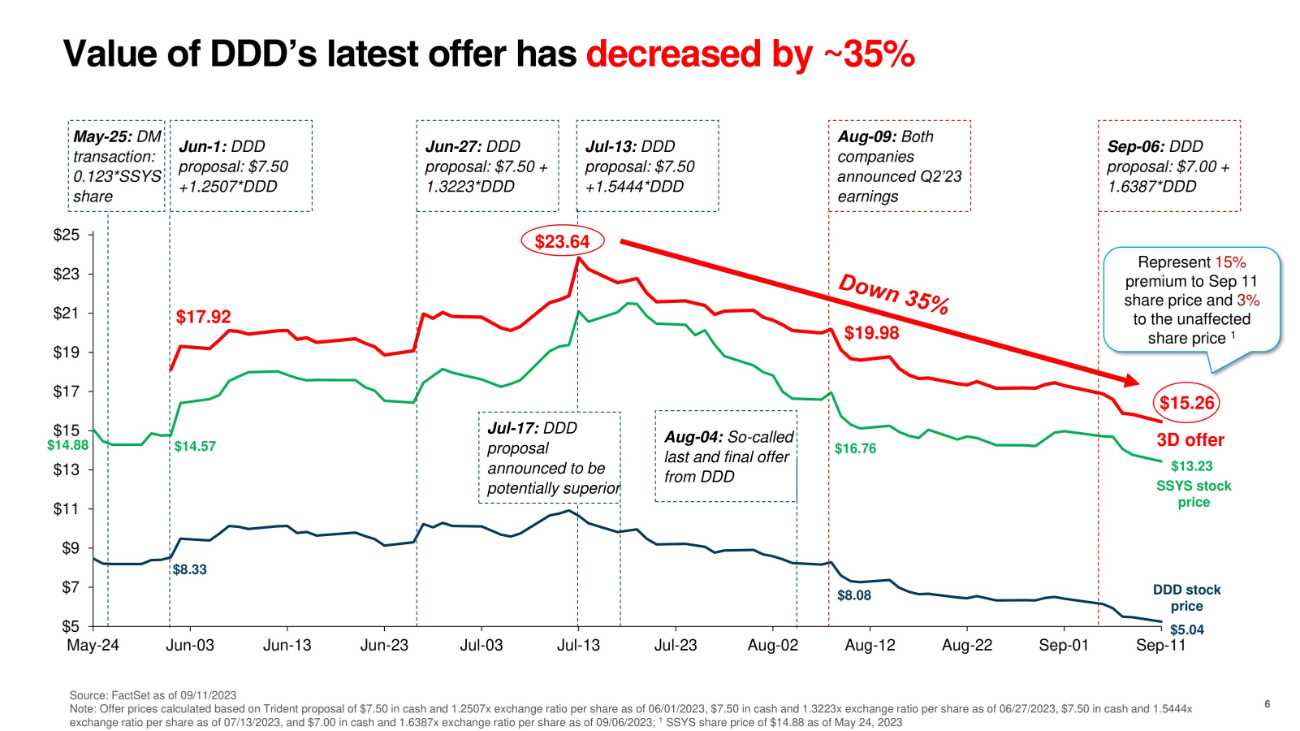

$5 $7 $9 $11 $15 $17 $19 $21 $23 $25 May - 24 Jun - 03 Jun - 13 Jun - 23 Jul - 03 Jul - 13 Jul - 23 Aug - 02 Aug - 12 Aug - 22 Sep - 01 Sep - 11 Jun - 1: DDD proposal: $7.50 +1.2507*DDD Value of DDD’s latest offer has decreased by ~35% 6 Source: FactSet as of 09/11/2023 Note: Offer prices calculated based on Trident proposal of $7.50 in cash and 1.2507x exchange ratio per share as of 06/01/2023, $7.50 in cash and 1.3223x exchange ratio per share as of 06/27/2023, $7.50 in cash and 1.5444x exchange ratio per share as of 07/13/2023, and $7.00 in cash and 1.6387x exchange ratio per share as of 09/06/2023; 1 SSYS share price of $14.88 as of May 24, 2023 Jul - 13: DDD proposal: $7.50 +1.5444*DDD Jun - 27: DDD proposal: $7.50 + 1.3223*DDD $15.26 $8.33 $16.76 $19.98 $8.08 $23.64 $14.88 $13 Jul - 17: DDD proposal announced to be potentially superior May - 25: DM transaction: 0.123*SSYS share $14.57 $17.92 Aug - 09: Both companies announced Q2’23 earnings Sep - 06: DDD proposal: $7.00 + 1.6387*DDD Represent 15% premium to Sep 11 share price and 3% to the unaffected share price 1 Aug - 04 : So - called last and final offer from DDD DDD stock price $5.04 3D offer $13.23 SSYS stock price

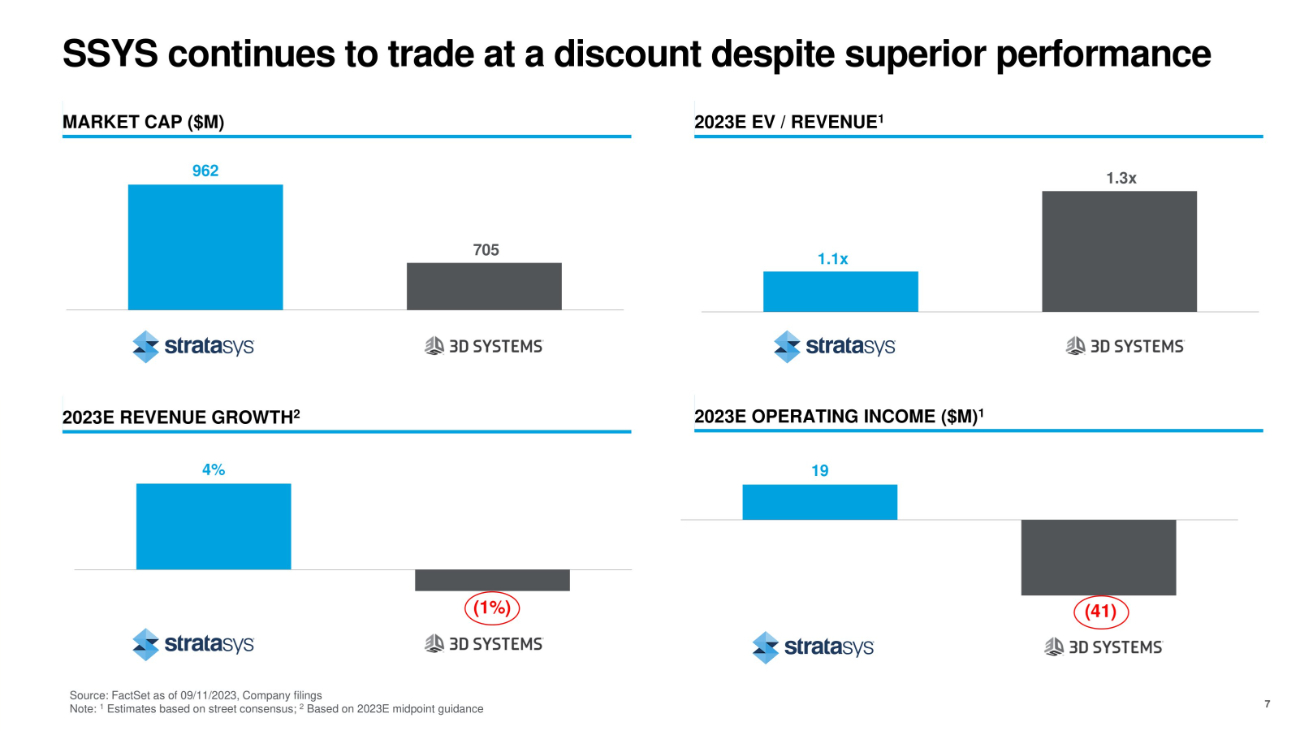

SSYS continues to trade at a discount despite superior performance MARKET CAP ($M) Source: FactSet as of 09/11/2023, Company filings Note: 1 Estimates based on street consensus; 2 Based on 2023E midpoint guidance 7 2023E REVENUE GROWTH 2 2023E EV / REVENUE 1 2023E OPERATING INCOME ($M) 1 962 705 1.1x 1.3x 4% 19 (41) (1%)

Agenda 8 DDD’s current proposal significantly undervalues SSYS 1 Serious concerns about DDD’s short - to - medium - term growth prospects 2 Structural challenges to a path to attractive profitability 3 Net synergy potential is materially lower than what DDD is broadcasting 4 Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months 5 Serious concerns regarding the ability of DDD’s management team to run a combined company 6

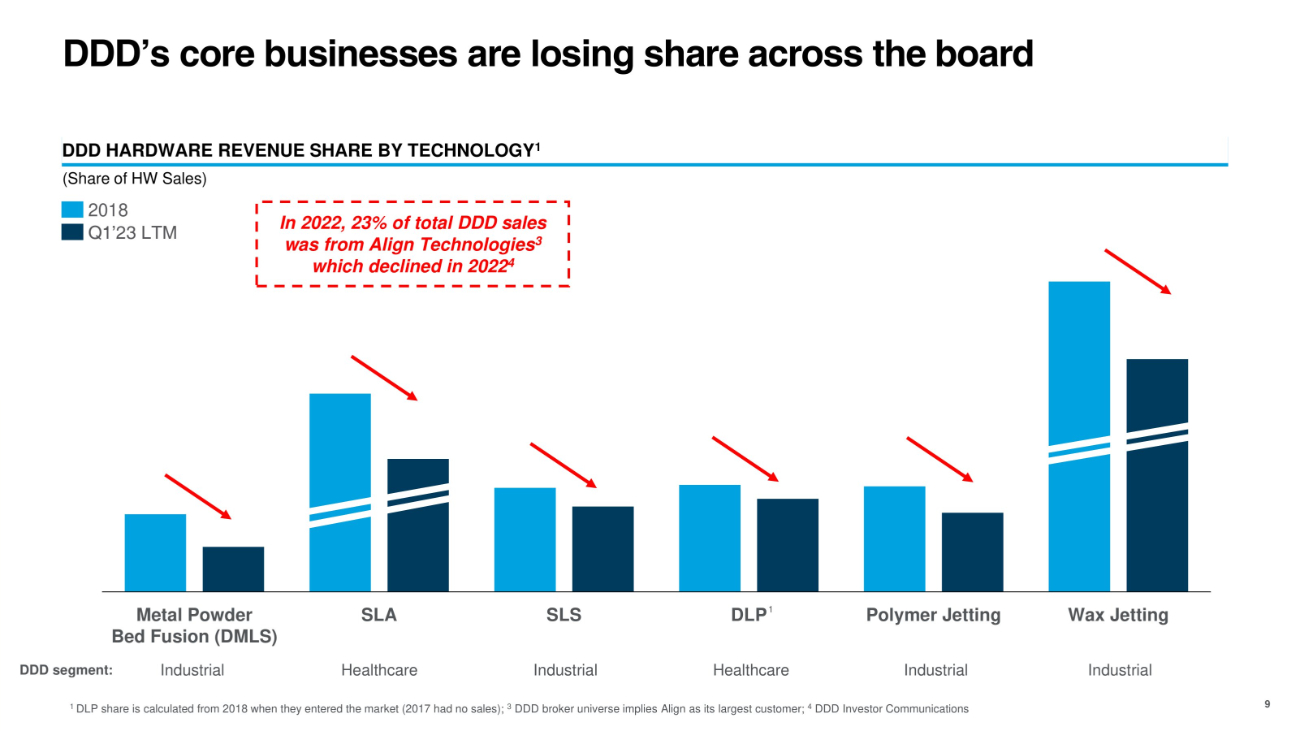

DDD’s core businesses are losing share across the board 9 DDD HARDWARE REVENUE SHARE BY TECHNOLOGY 1 Metal Powder Bed Fusion (DMLS) SLA SLS DLP 1 Polymer Jetting Wax Jetting 1 DLP share is calculated from 2018 when they entered the market (2017 had no sales); 3 DDD broker universe implies Align as its largest customer; 4 DDD Investor Communications (Share of HW Sales) 2018 Q1’23 LTM In 2022, 23% of total DDD sales was from Align Technologies 3 which declined in 2022 4 DDD segment: Industrial Healthcare Industrial Healthcare Industrial Industrial

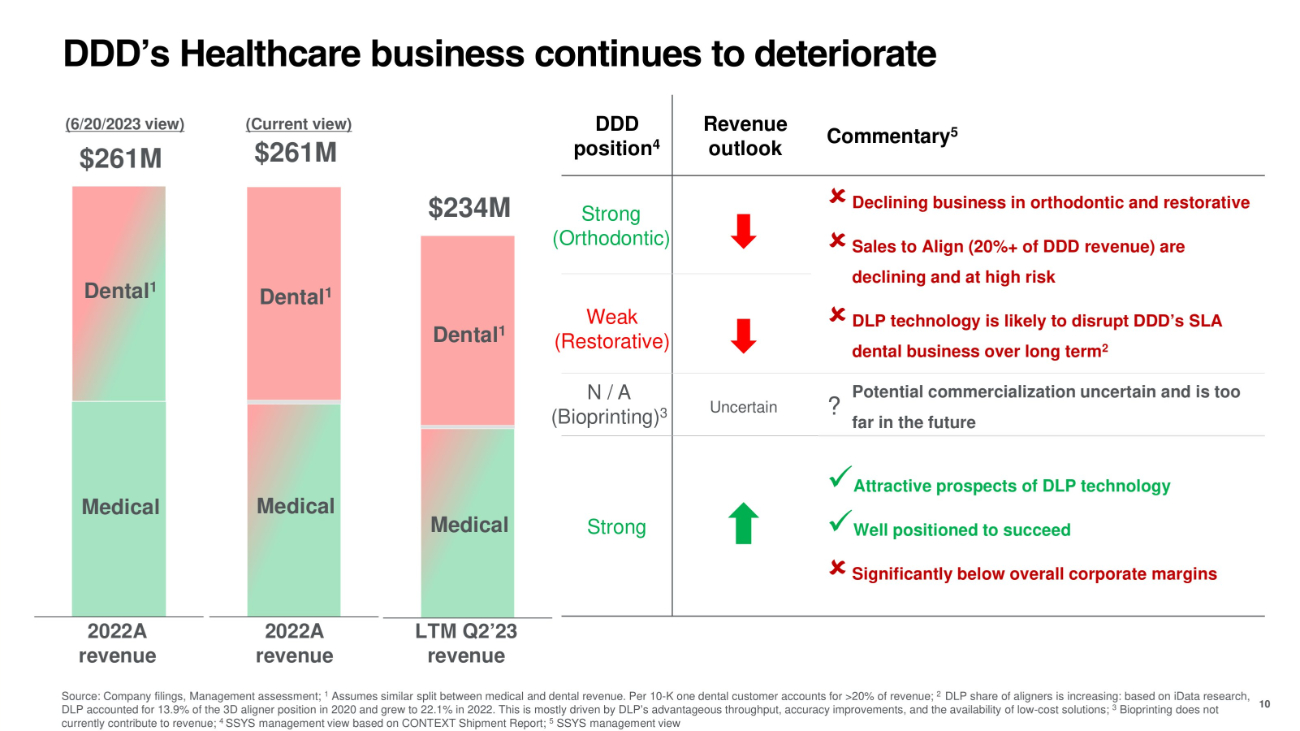

DDD’s Healthcare business continues to deteriorate Medical 2022A revenue 10 Dental 1 Source: Company filings, Management assessment; 1 Assumes similar split between medical and dental revenue. Per 10 - K one dental customer accounts for >20% of revenue; 2 DLP share of aligners is increasing: based on iData research, DLP accounted for 13.9% of the 3D aligner position in 2020 and grew to 22.1% in 2022. This is mostly driven by DLP’s advantageous throughput, accuracy improvements, and the availability of low - cost solutions; 3 Bioprinting does not currently contribute to revenue; 4 SSYS management view based on CONTEXT Shipment Report; 5 SSYS management view ( (6/20/2023 view) $261M Medical Dental 1 2022A revenue $234M ( ( Commentary 5 Revenue outlook DDD position 4 Declining business in orthodontic and restorative Sales to Align (20%+ of DDD revenue) are declining and at high risk DLP technology is likely to disrupt DDD’s SLA dental business over long term 2 Strong Orthodontic ) Weak Restorative) Potential commercialization uncertain and is too Uncertain ? far in the future N / A Bioprinting) 3 x Attractive prospects of DLP technology x Well positioned to succeed Significantly below overall corporate margins Strong (Current view) $261M Medical Dental 1 LTM Q2’23 revenue

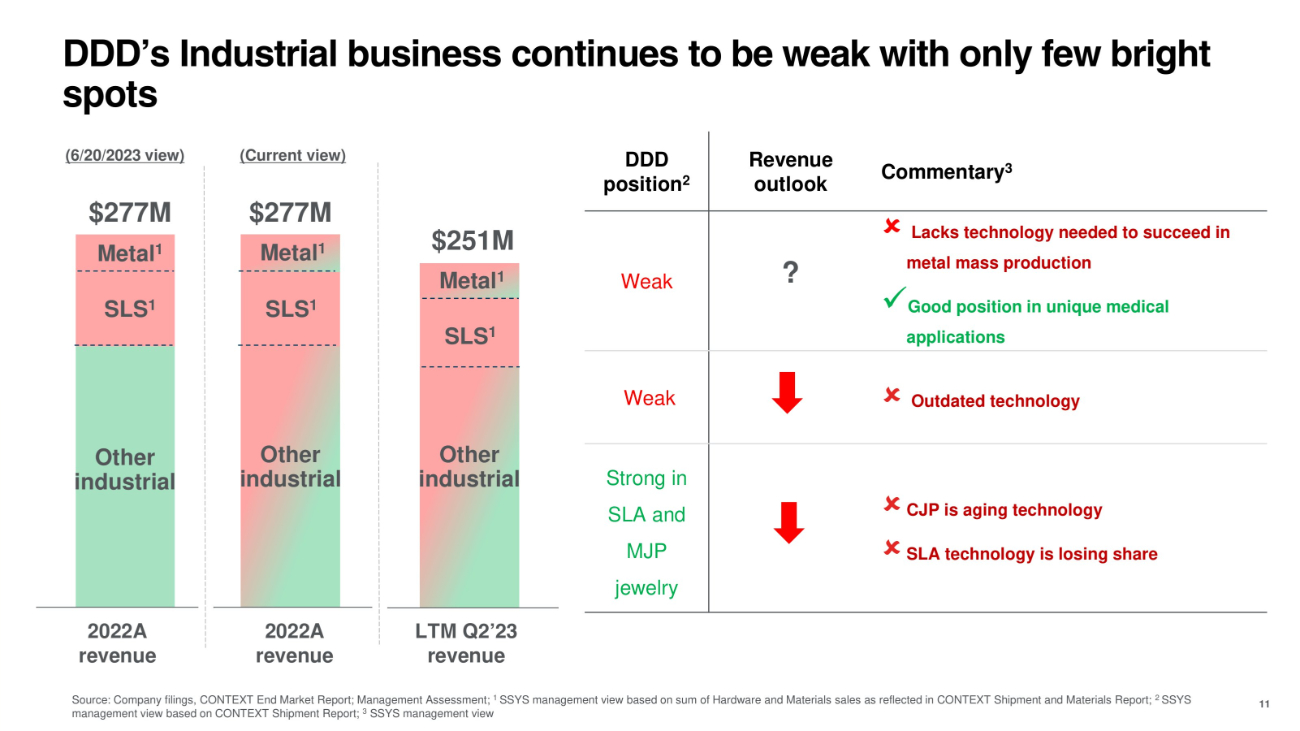

Metal 1 SLS 1 Other industrial Commentary 3 Revenue outlook DDD position 2 Lacks technology needed to succeed in ? metal mass production x Good position in unique medical applications Weak Outdated technology Weak CJP is aging technology SLA technology is losing share Strong in SLA and MJP jewelry DDD’s Industrial business continues to be weak with only few bright spots 11 Source: Company filings, CONTEXT End Market Report; Management Assessment; 1 SSYS management view based on sum of Hardware and Materials sales as reflected in CONTEXT Shipment and Materials Report; 2 SSYS management view based on CONTEXT Shipment Report; 3 SSYS management view Metal 1 SLS 1 Other industrial $277M $277M 2022A revenue 2022A revenue LTM Q2’23 revenue Metal 1 SLS 1 Other industrial $251M (6/20/2023 view) (Current view)

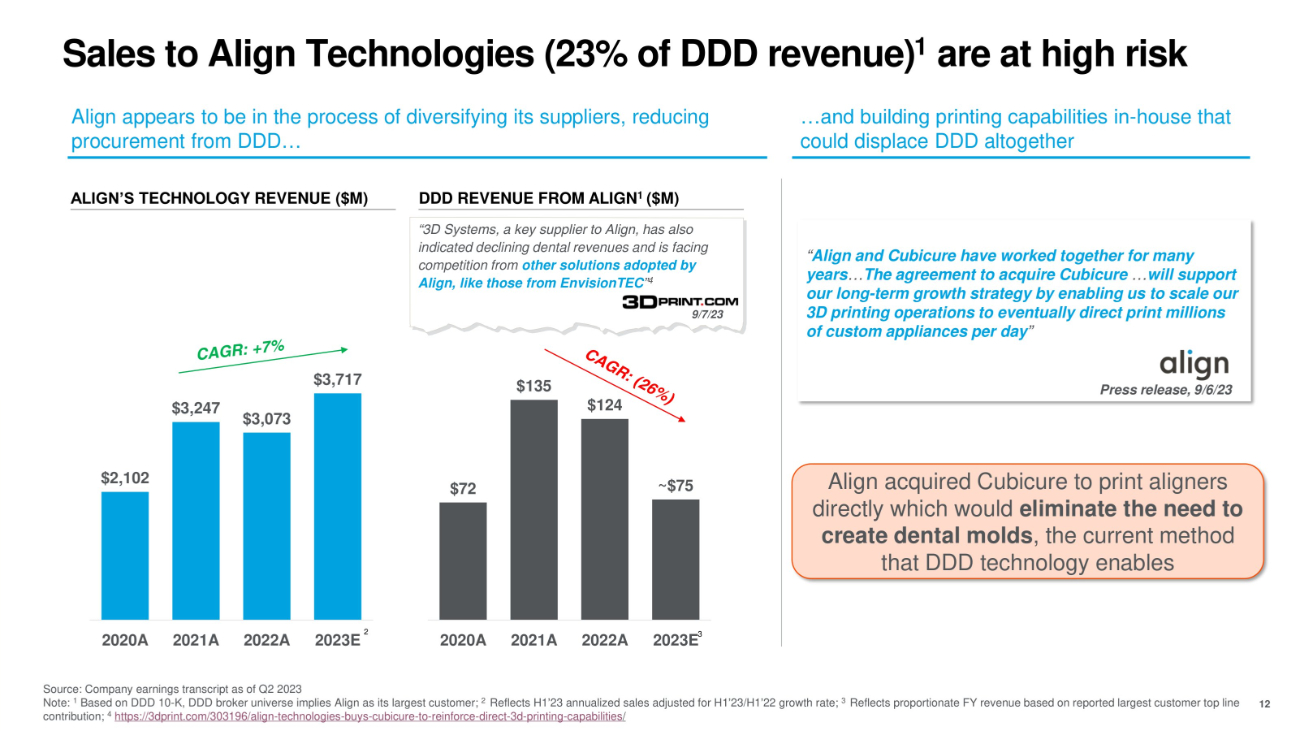

Sales to Align Technologies (23% of DDD revenue) 1 are at high risk $72 $135 $124 ~$75 2020A 2021A 2022A 2023E 3 $2,102 $3,247 $3,073 $3,717 2 2020A 2021A 2022A 2023E ALIGN’S TECHNOLOGY REVENUE ($M) DDD REVENUE FROM ALIGN 1 ($M) Align appears to be in the process of diversifying its suppliers, reducing procurement from DDD… …and building printing capabilities in - house that could displace DDD altogether Align acquired Cubicure to print aligners directly which would eliminate the need to create dental molds , the current method that DDD technology enables Source: Company earnings transcript as of Q2 2023 Note: 1 Based on DDD 10 - K, DDD broker universe implies Align as its largest customer; 2 Reflects H1’23 annualized sales adjusted for H1’23/H1’22 growth rate; 3 Reflects proportionate FY revenue based on reported largest customer top line contribution; 4 https://3dprint.com/303196/align - technologies - buys - cubicure - to - reinforce - direct - 3d - printing - capabilities / “3D Systems, a key supplier to Align, has also indicated declining dental revenues and is facing competition from other solutions adopted by Align, like those from EnvisionTEC ” 4 12 9/7/23 “ Align and Cubicure have worked together for many years … The agreement to acquire Cubicure … will support our long - term growth strategy by enabling us to scale our 3D printing operations to eventually direct print millions of custom appliances per day ” Press release, 9/6/23

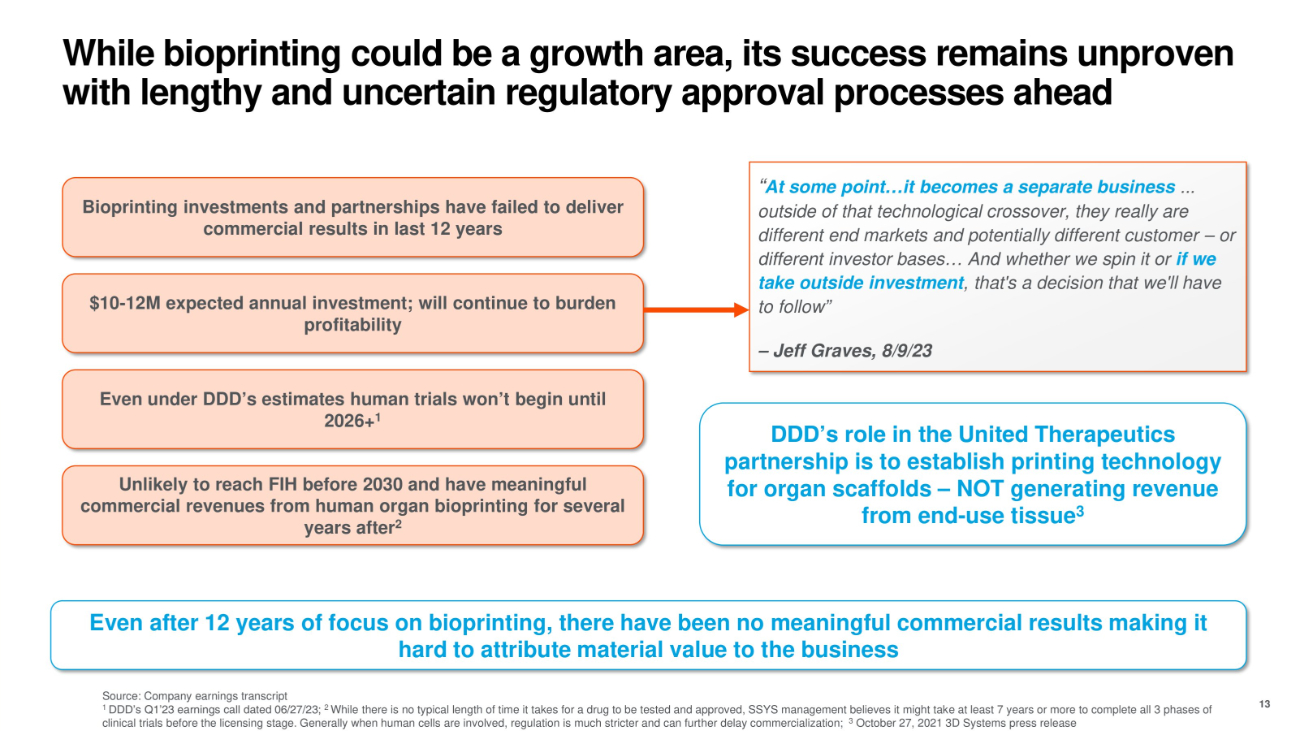

While bioprinting could be a growth area, its success remains unproven with lengthy and uncertain regulatory approval processes ahead 13 Even after 12 years of focus on bioprinting, there have been no meaningful commercial results making it hard to attribute material value to the business Bioprinting investments and partnerships have failed to deliver commercial results in last 12 years $10 - 12M expected annual investment; will continue to burden profitability Even under DDD’s estimates human trials won’t begin until 2026+ 1 “ At some point…it becomes a separate business ... outside of that technological crossover, they really are different end markets and potentially different customer – or different investor bases… And whether we spin it or if we take outside investment , that's a decision that we'll have to follow” – Jeff Graves, 8/9/23 Source: Company earnings transcript 1 DDD’s Q1’23 earnings call dated 06/27/23; 2 While there is no typical length of time it takes for a drug to be tested and approved, SSYS management believes it might take at least 7 years or more to complete all 3 phases of clinical trials before the licensing stage. Generally when human cells are involved, regulation is much stricter and can further delay commercialization; 3 October 27, 2021 3D Systems press release Unlikely to reach FIH before 2030 and have meaningful commercial revenues from human organ bioprinting for several years after 2 DDD’s role in the United Therapeutics partnership is to establish printing technology for organ scaffolds – NOT generating revenue from end - use tissue 3

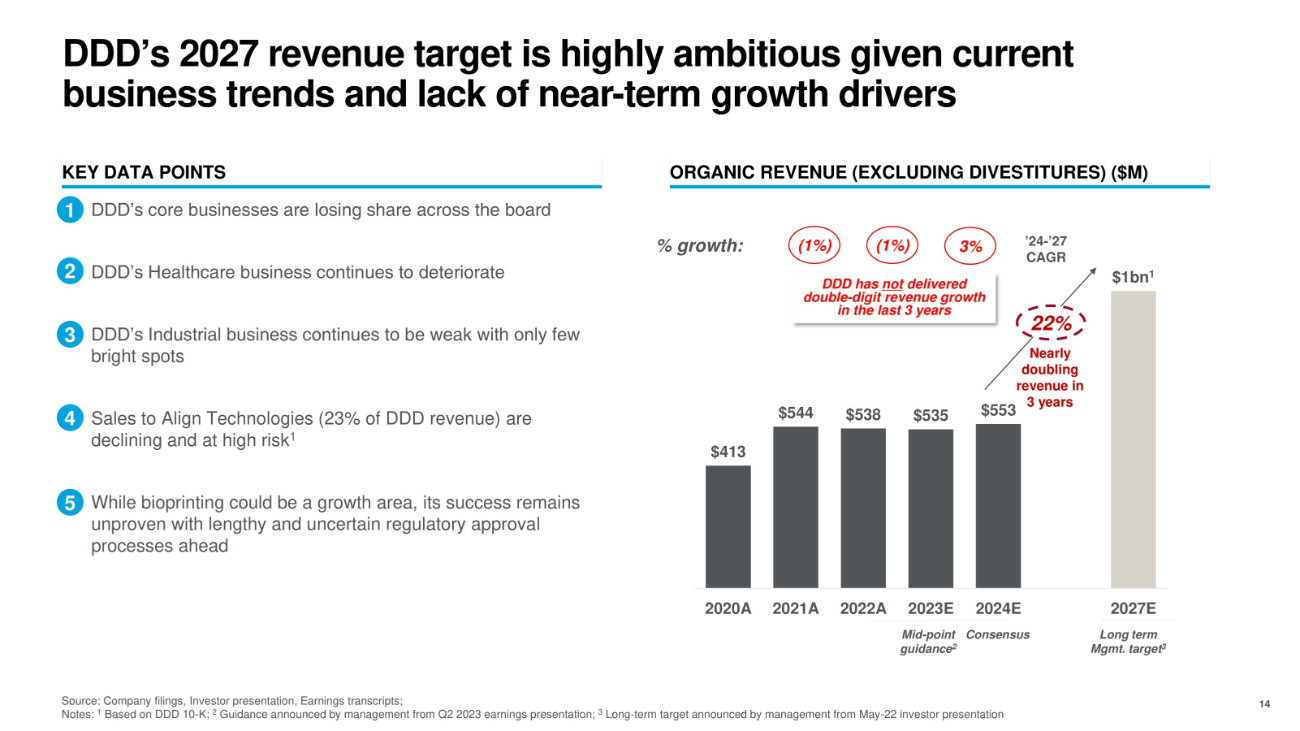

$413 $544 $538 $535 $553 $1bn 1 2020A 2021A 2022A 2023E 2024E 2027E DDD’s 2027 revenue target is highly ambitious given current business trends and lack of near - term growth drivers KEY DATA POINTS ORGANIC REVENUE (EXCLUDING DIVESTITURES) ($M) 14 % growth: ’24 - ’27 CAGR (1%) (1%) 3% 22% Nearly doubling revenue in 3 years Consensus Source: Company filings, Investor presentation, Earnings transcripts; Notes: 1 Based on DDD 10 - K; 2 Guidance announced by management from Q2 2023 earnings presentation; 3 Long - term target announced by management from May - 22 investor presentation Long term Mgmt. target 3 Mid - point guidance 2 Sales to Align Technologies (23% of DDD revenue) are declining and at high risk 1 1 ؘ DDD’s core businesses are losing share across the board 2 ؘ DDD’s Healthcare business continues to deteriorate 3 ؘ DDD’s Industrial business continues to be weak with only few bright spots 4 ؘ 5 ؘ While bioprinting could be a growth area, its success remains unproven with lengthy and uncertain regulatory approval processes ahead DDD has not delivered double - digit revenue growth in the last 3 years

Agenda 15 DDD’s current proposal significantly undervalues SSYS 1 Serious concerns about DDD’s short - to - medium - term growth prospects 2 Structural challenges to a path to attractive profitability 3 Net synergy potential is materially lower than what DDD is broadcasting 4 Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months 5 Serious concerns regarding the ability of DDD’s management team to run a combined company 6

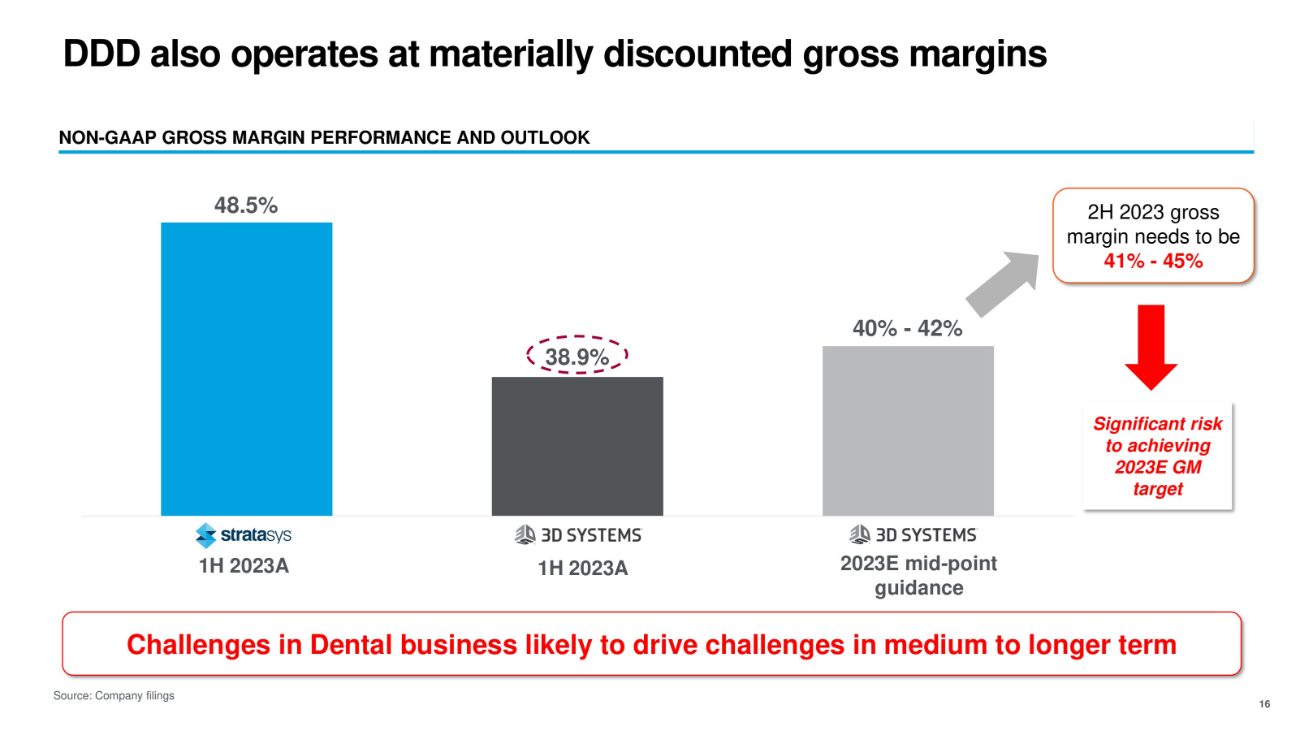

DDD also operates at materially discounted gross margins 16 NON - GAAP GROSS MARGIN PERFORMANCE AND OUTLOOK Source: Company filings Challenges in Dental business likely to drive challenges in medium to longer term 48.5% 1H 2023A 1H 2023A 38.9% Significant risk to achieving 2023E GM target 2023E mid - point guidance 2H 2023 gross margin needs to be 41% - 45% 40% - 42%

Agenda 17 DDD’s current proposal significantly undervalues SSYS 1 Serious concerns about DDD’s short - to - medium - term growth prospects 2 Structural challenges to a path to attractive profitability 3 Net synergy potential is materially lower than what DDD is broadcasting 4 Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months 5 Serious concerns regarding the ability of DDD’s management team to run a combined company 6

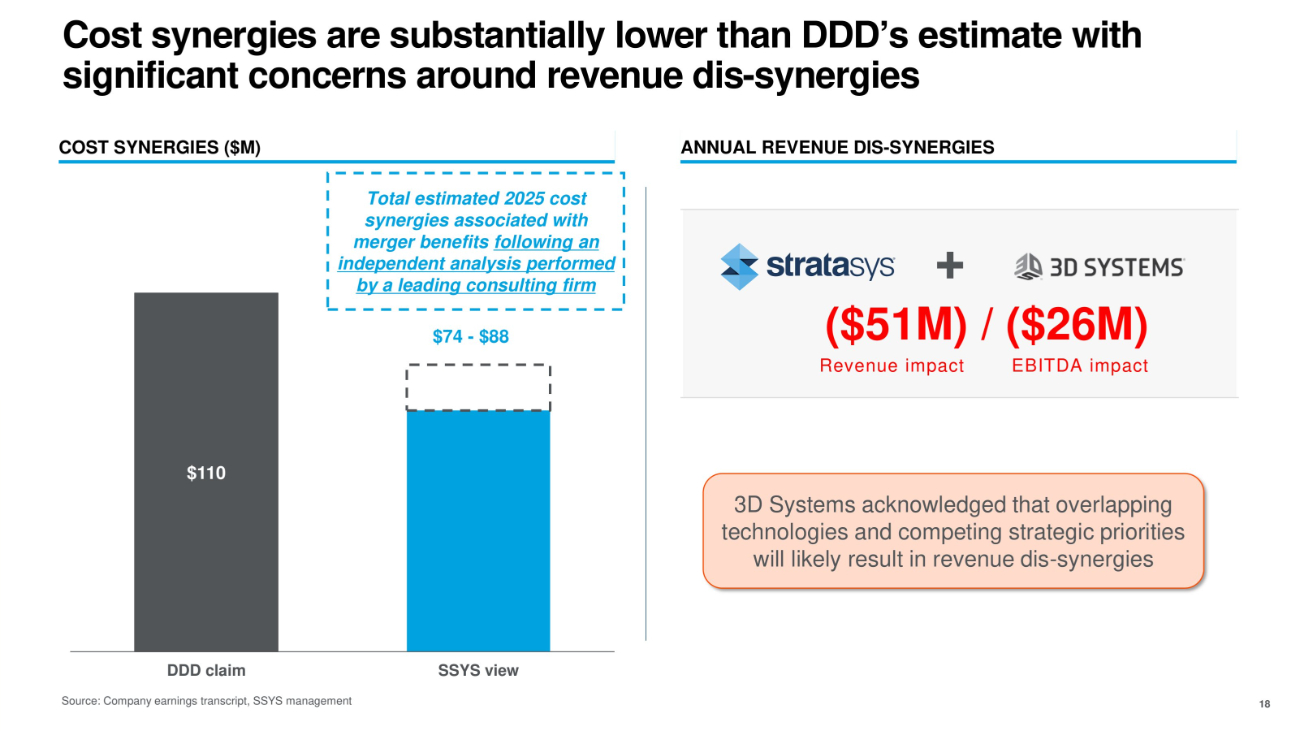

Cost synergies are substantially lower than DDD’s estimate with significant concerns around revenue dis - synergies COST SYNERGIES ($M) ANNUAL REVENUE DIS - SYNERGIES $110 DDD claim SSYS view $74 - $88 + ($51M) / ($26M) Revenue impact EBITDA impact Total estimated 2025 cost synergies associated with merger benefits following an independent analysis performed by a leading consulting firm 18 Source: Company earnings transcript, SSYS management 3D Systems acknowledged that overlapping technologies and competing strategic priorities will likely result in revenue dis - synergies

Agenda 19 DDD’s current proposal significantly undervalues SSYS 1 Serious concerns about DDD’s short - to - medium - term growth prospects 2 Structural challenges to a path to attractive profitability 3 Net synergy potential is materially lower than what DDD is broadcasting 4 Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months 5 Serious concerns regarding the ability of DDD’s management team to run a combined company 6

Extended regulatory review could have adverse impact on both businesses ⚫ There is a high risk of a lengthy and extensive regulatory review process for a transaction with DDD. If the transaction were to close, then it has potential to take 9 - 18 months ⚫ The significantly elongated timeline to close increases the risk of key employee attrition ⚫ Customers and channel partner disruption is expected ⚫ Severe limitations on ability of SSYS to pursue other acquisition opportunities during long pendency of the transaction 20

Agenda 21 DDD’s current proposal significantly undervalues SSYS 1 Serious concerns about DDD’s short - to - medium - term growth prospects 2 Structural challenges to a path to attractive profitability 3 Net synergy potential is materially lower than what DDD is broadcasting 4 Significant regulatory consummation risks and extended timeline to closing of 9 to 18 months 5 Serious concerns regarding the ability of DDD’s management team to run a combined company 6

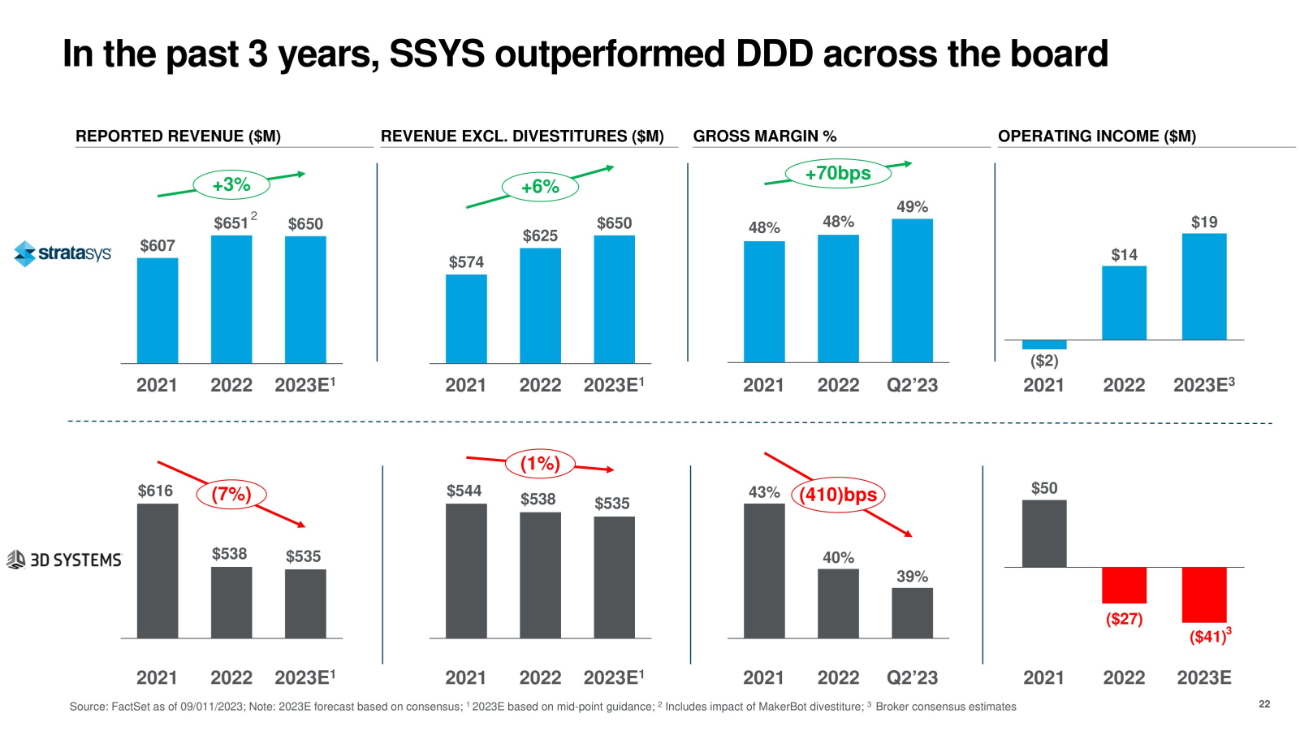

In the past 3 years, SSYS outperformed DDD across the board 2021 2022 Q2’23 48% 48% 49% +70bps $14 ($2) 2021 2022 2023E 3 $19 43% 40% 39% (410)bps $607 $651 2 $650 2021 2022 2023E 1 +3% $616 $538 $535 (7%) $574 $625 $650 2021 2022 2023E 1 +6% $544 $538 $535 (1%) 2021 2022 2023E 1 2021 2022 2023E 1 2021 2022 Q2’23 Source: FactSet as of 09/011/2023; Note: 2023E forecast based on consensus; 1 2023E based on mid - point guidance; 2 Includes impact of MakerBot divestiture; 3 Broker consensus estimates $50 ($27) ($41) 3 2021 2022 2023E REPORTED REVENUE ($M) REVENUE EXCL. DIVESTITURES ($M) GROSS MARGIN % OPERATING INCOME ($M) 22

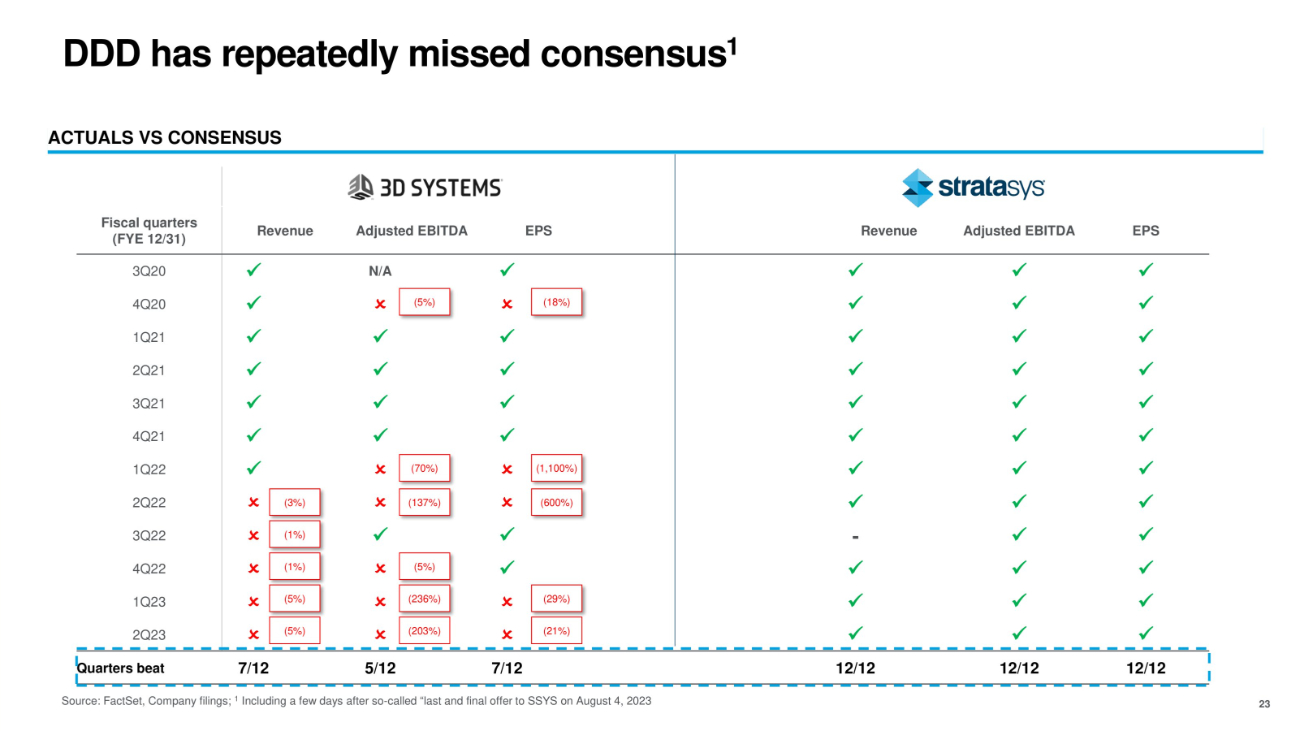

DDD has repeatedly missed consensus 1 23 ACTUALS VS CONSENSUS EPS Adjusted EBITDA Revenue EPS Adjusted EBITDA Revenue Fiscal quarters (FYE 12/31) x x x x N/A x 3Q20 x x x X (18%) X (5%) x 4Q20 x x x x x x 1Q21 x x x x x x 2Q21 x x x x x x 3Q21 x x x x x x 4Q21 x x x X (1,100%) X (70%) x 1Q22 x x x X (600%) X (137%) X (3%) 2Q22 x x - x x X (1%) 3Q22 x x x x X (5%) X (1%) 4Q22 x x x X (29%) X (236%) X (5%) 1Q23 x x x X (21%) X (203%) X (5%) 2Q23 12/12 12/12 12/12 7/12 5/12 7/12 Quarters beat Source: FactSet, Company filings; 1 Including a few days after so - called “last and final offer to SSYS on August 4, 2023

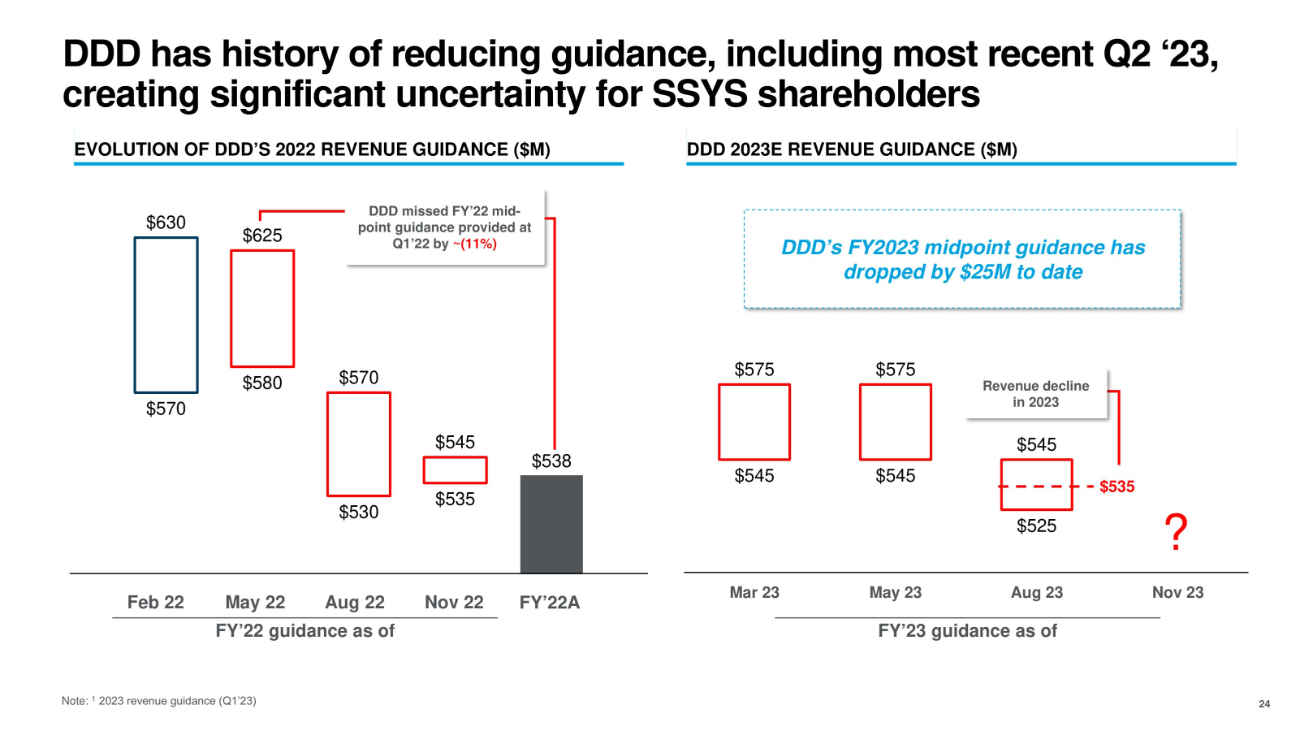

DDD has history of reducing guidance, including most recent Q2 ‘23, creating significant uncertainty for SSYS shareholders 24 $570 $580 $530 $535 $538 $630 $625 $570 $545 Feb 22 May 22 Aug 22 FY’22 guidance as of Nov 22 FY’22A DDD missed FY’22 mid - point guidance provided at Q1’22 by ~(11%) EVOLUTION OF DDD’S 2022 REVENUE GUIDANCE ($M) DDD 2023E REVENUE GUIDANCE ($M) $545 $545 $525 $575 $575 $545 Mar 23 May 23 Aug 23 FY’23 guidance as of Nov 23 $535 DDD’s FY2023 midpoint guidance has dropped by $25M to date Revenue decline in 2023 ? Note: 1 2023 revenue guidance (Q1’23)

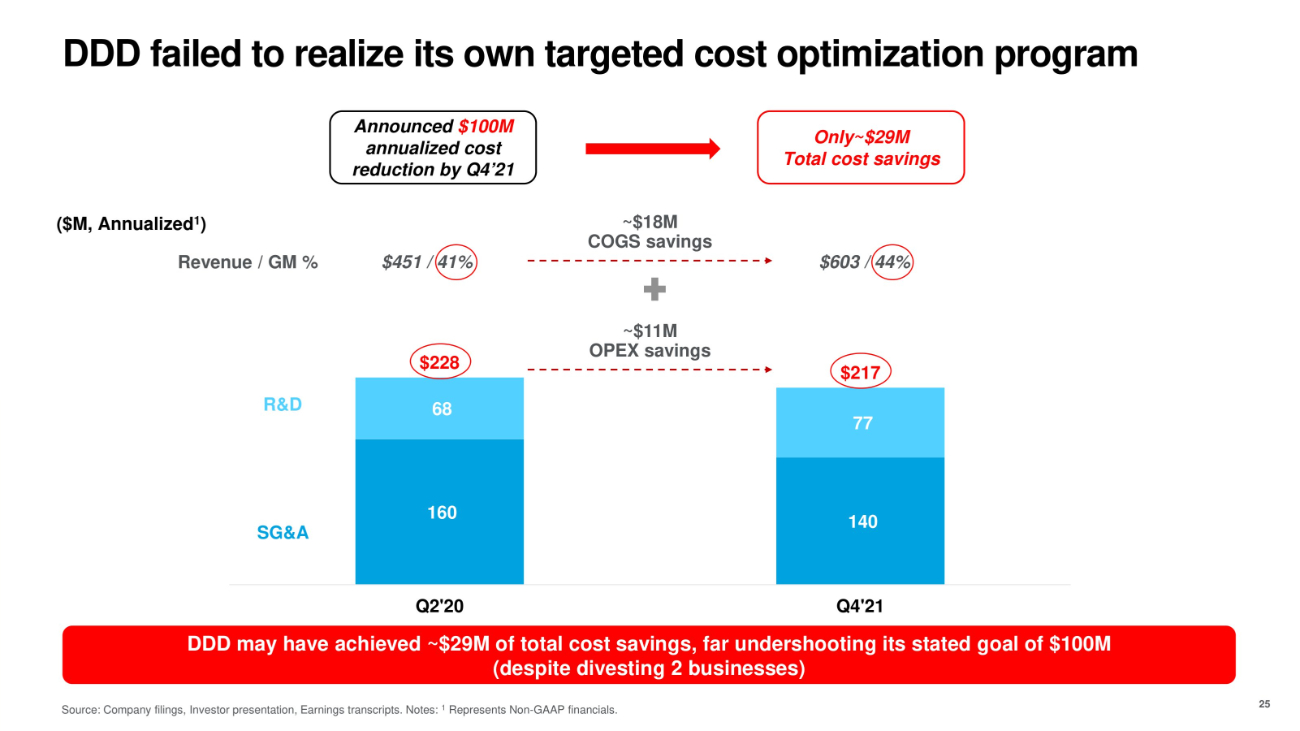

DDD failed to realize its own targeted cost optimization program Source: Company filings, Investor presentation, Earnings transcripts. Notes: 1 Represents Non - GAAP financials. 25 Announced $100M annualized cost reduction by Q4’21 ($M, Annualized 1 ) 160 140 68 77 $228 $217 Q2'20 Q4'21 DDD may have achieved ~$29M of total cost savings, far undershooting its stated goal of $100M (despite divesting 2 businesses) SG&A R&D Revenue / GM % $451 / 41% $603 / 44% ~$18M COGS savings ~$11M OPEX savings Only~$29M Total cost savings

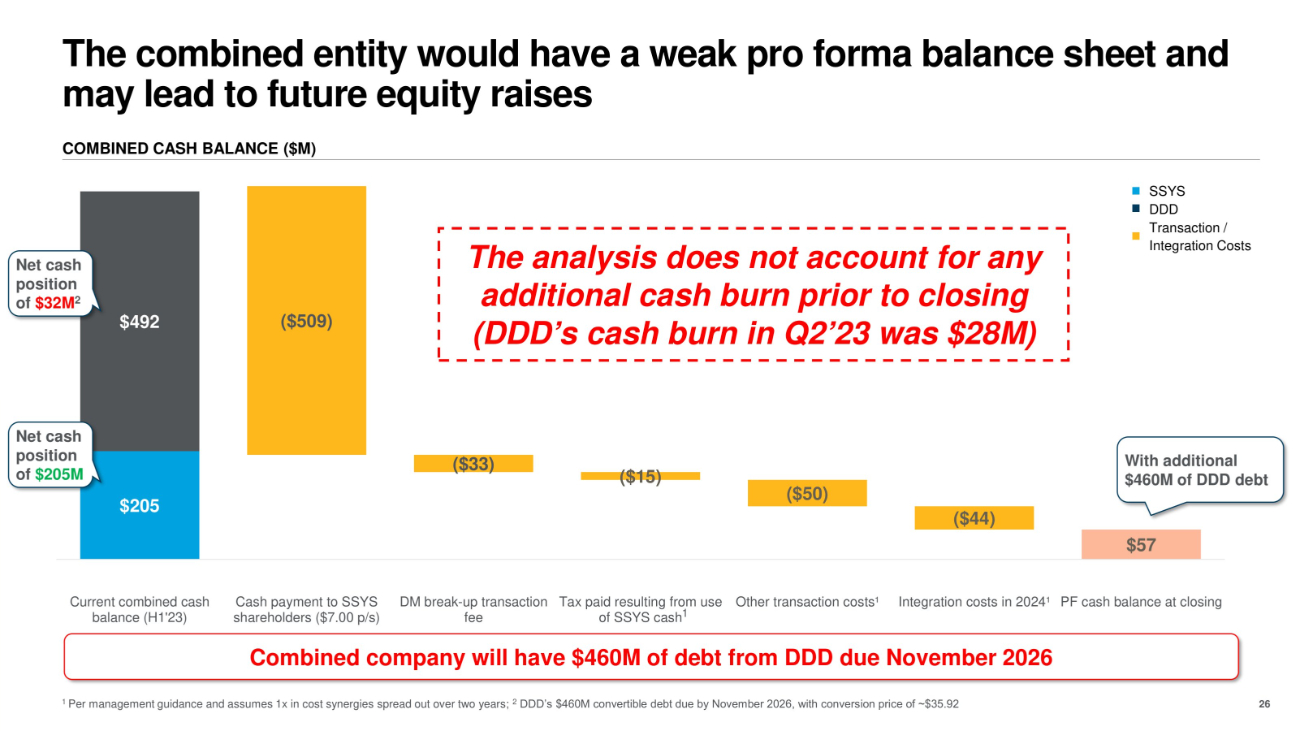

The combined entity would have a weak pro forma balance sheet and may lead to future equity raises $205 ($509) ($33) ($15) ($50) ($44) $57 $492 Current combined cash balance (H1'23) Cash payment to SSYS shareholders ($7.00 p/s) DM break - up transaction Tax paid resulting from use Other transaction costs¹ fee of SSYS cash 1 Integration costs in 2024¹ PF cash balance at closing 26 1 Per management guidance and assumes 1x in cost synergies spread out over two years; 2 DDD’s $460M convertible debt due by November 2026, with conversion price of ~$35.92 SSYS DDD Transaction / Integration Costs COMBINED CASH BALANCE ($M) The analysis does not account for any additional cash burn prior to closing (DDD’s cash burn in Q2’23 was $28M) Combined company will have $460M of debt from DDD due November 2026 Net cash position of $205M Net cash position of $32M 2 With additional $460M of DDD debt

HIGHLY PRELIMINARY DRAFT – SUBJECT TO REVISION Disclaimer 27 Forward - Looking Statements This document contains forward - looking statements that involve risks, uncertainties and assumptions. If the risks or uncertainties ever materialize or the assumptions prove incorrect, the actual results of Stratasys Ltd. and its consolidated subsidiaries (“Stratasys”) may differ materially from those expressed or implied by such forward - looking statements and assumptions. All statements other than statements of historical fact are statements that could be deemed forward - looking statements. Such forward - looking statements include statements relating to the proposed transaction between Stratasys and Desktop Metal, Inc. (“Desktop Metal”), including statements regarding the benefits of the transaction and the anticipated timing of the transaction, and information regarding the businesses of Stratasys and Desktop Metal, including expectations regarding outlook and all underlying assumptions, Stratasys’ and Desktop Metal’s objectives, plans and strategies, information relating to operating trends in markets where Stratasys and Desktop Metal operate, statements that contain projections of results of operations or of financial condition and all other statements other than statements of historical fact that address activities, events or developments that Stratasys or Desktop Metal intends, expects, projects, believes or anticipates will or may occur in the future. Such statements are based on management’s beliefs and assumptions made based on information currently available to management. All statements in this communication, other than statements of historical fact, are forward - looking statements that may be identified by the use of the words “outlook,” “guidance,” “expects,” “believes,” “anticipates,” “should,” “estimates,” and similar expressions. These forward - looking statements involve known and unknown risks and uncertainties, which may cause Stratasys’ or Desktop Metal’s actual results and performance to be materially different from those expressed or implied in the forward - looking statements. Factors and risks that may impact future results and performance include, but are not limited to those factors and risks described in Item 3.D “Key Information - Risk Factors”, Item 4 “Information on the Company”, and Item 5 “Operating and Financial Review and Prospects” in Stratasys’ Annual Report on Form 20 - F for the year ended December 31, 2022 and Part 1, Item 1A, “Risk Factors” in Desktop Metal’s Annual Report on Form 10 - K for the year ended December 31, 2022, each filed with the Securities and Exchange Commission (the “SEC”), and in other filings by Stratasys and Desktop Metal with the SEC. These include, but are not limited to: factors relating to actions taken by or other developments involving Nano Dimension Ltd. (“Nano”), including any future unsolicited tender offer similar to its recently - expired partial tender offer for shares of Stratasys or Nano’s legal challenge to Stratasys’ shareholder rights plan, and actions taken by Stratasys or its shareholders with respect to such actions or developments, the ultimate outcome of the proposed transaction between Stratasys and Desktop Metal, including the possibility that Stratasys or Desktop Metal shareholders will reject the proposed transaction; the effect of the announcement of the proposed transaction on the ability of Stratasys and Desktop Metal to operate their respective businesses and retain and hire key personnel and to maintain favorable business relationships; the timing of the proposed transaction; the occurrence of any event, change or other circumstance that could give rise to the termination of the proposed transaction; the ability to satisfy closing conditions to the completion of the proposed transaction (including any necessary shareholder approvals); other risks related to the completion of the proposed transaction and actions related thereto; changes in demand for Stratasys’ or Desktop Metal’s products and services; global market, political and economic conditions, and in the countries in which Stratasys and Desktop Metal operate in particular; government regulations and approvals; the extent of growth of the 3D printing market generally; the global macro - economic environment, including headwinds caused by inflation, rising interest rates, unfavorable currency exchange rates and potential recessionary conditions; the impact of shifts in prices or margins of the products that Stratasys or Desktop Metal sells or services Stratasys or Desktop Metal provides, including due to a shift towards lower margin products or services; the potential adverse impact that recent global interruptions and delays involving freight carriers and other third parties may have on Stratasys’ or Desktop Metal’s supply chain and distribution network and consequently, Stratasys’ or Desktop Metal’s ability to successfully sell both existing and newly - launched 3D printing products; litigation and regulatory proceedings, including any proceedings that may be instituted against Stratasys or Desktop Metal related to the proposed transaction; impacts of rapid technological change in the additive manufacturing industry, which requires Stratasys and Desktop Metal to continue to develop new products and innovations to meet constantly evolving customer demands and which could adversely affect market adoption of Stratasys’ or Desktop Metal’s products; and disruptions of Stratasys’ or Desktop Metal’s information technology systems. These risks, as well as other risks related to the proposed transaction, are included in the registration statement on Form F - 4 and joint proxy statement/prospectus that has been filed with the Securities and Exchange Commission (“SEC”) in connection with the proposed transaction. While the list of factors presented here is, and the list of factors presented in the registration statement on Form F - 4 are, considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. For additional information about other factors that could cause actual results to differ materially from those described in the forward - looking statements, please refer to Stratasys’ and Desktop Metal’s respective periodic reports and other filings with the SEC, including the risk factors identified in Stratasys’ and Desktop Metal’s Annual Reports on Form 20 - F and Form 10 - K, respectively, and Stratasys’ Form 6 - K reports that published its results for the quarter ended March 31, 2023, which it furnished to the SEC on May 16, 2023, and Desktop Metal’s most recent Quarterly Reports on Form 10 - Q. The forward - looking statements included in this communication are made only as of the date hereof. Neither Stratasys nor Desktop Metal undertakes any obligation to update any forward - looking statements to reflect subsequent events or circumstances, except as required by law. No Offer or Solicitation This communication is not intended to and shall not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made, except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended.

HIGHLY PRELIMINARY DRAFT – SUBJECT TO REVISION Disclaimer 28 Important Additional Information In connection with the proposed transaction, Stratasys filed with the SEC a registration statement on Form F - 4 that includes a joint proxy statement of Stratasys and Desktop Metal and that also constitutes a prospectus of Stratasys. Each of Stratasys and Desktop Metal may also file other relevant documents with the SEC regarding the proposed transaction. The registration statement was declared effective by the SEC on August 25, 2023. Stratasys filed the definitive proxy statement/prospectus with the SEC on August 28, 2023. The definitive proxy statement/prospectus was mailed to shareholders of Stratasys and Desktop Metal on or around August 28, 2023. Each of Stratasys and Desktop Metal may also file other relevant documents with the SEC regarding the proposed transaction. This document is not a substitute for the definitive proxy statement/prospectus or any other document that Stratasys or Desktop Metal may file with the SEC. This document is not a substitute for the joint proxy statement/prospectus or registration statement or any other document that Stratasys or Desktop Metal may file with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT, THE JOINT PROXY STATEMENT/PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS THAT MAY BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain free copies of the registration statement and definitive joint proxy statement/prospectus and other documents containing important information about Stratasys, Desktop Metal and the proposed transaction, once such documents are filed with the SEC through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with, or furnished, to the SEC by Stratasys will be available free of charge on Stratasys’ website at https://investors.stratasys.com/sec - filings. Copies of the documents filed with the SEC by Desktop Metal will be available free of charge on Desktop Metal’s website at https://ir.desktopmetal.com/sec - filings/all - sec - filings. Participants in the Solicitation Stratasys, Desktop Metal and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information about the directors and executive officers of Stratasys, including a description of their direct or indirect interests, by security holdings or otherwise, is set forth in Stratasys’ proxy statement for its 2023 Annual General Meeting of Shareholders, which was filed with the SEC on July 12, 2023, and Stratasys’ Annual Report on Form 20 - F for the fiscal year ended December 31, 2022, which was filed with the SEC on March 3, 2023. Information about the directors and executive officers of Desktop Metal, including a description of their direct or indirect interests, by security holdings or otherwise, is set forth in Desktop Metal’s proxy statement for its 2023 Annual Meeting of Stockholders, which was filed with the SEC on April 25, 2023 and Desktop Metal’s Annual Report on Form 10 - K for the fiscal year ended December 31, 2022, which was filed with the SEC on March 1, 2023. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, is contained in the joint proxy statement/prospectus and other relevant materials filed with the SEC regarding the proposed transaction. Investors should read the joint proxy statement/prospectus carefully before making any voting or investment decisions. You may obtain free copies of these documents from Stratasys or Desktop Metal using the sources indicated above. Use of Non - GAAP Financial Measures This communication contains certain forward - looking non - GAAP measures, which are based on internal forecasts and represent management’s best judgment. Reconciliation of such measures to the most directly comparable GAAP financial measures cannot be furnished without unreasonable efforts due to inherent difficulty in forecasting the amount and timing of certain adjustments that are necessary for such reconciliations and which may significantly impact our GAAP results. [In particular, sufficient information is not available to calculate certain adjustments that are required to prepare a forward - looking statement of revenue, margin and EBITDA in accordance with GAAP for fiscal years 2024 and beyond. Stratasys also believes that such reconciliations would also imply a degree of precision that would be confusing or inappropriate for these forward - looking measures, which are inherently uncertain.] All revenue, margin, EBITDA and other P&L references are non - GAAP unless specified otherwise.